IHS Markit (NASDAQ: INFO) had a hugely successful fiscal year 2019 (ending November), with strong revenue growth across segments driving steady improvement in profits. This helped the company’s stock jump 65% from $48 in January to around $79 now. Moreover, the company’s adjusted EBITDA margin also widened by 120 basis points due to lower operating expenses.

However, we believe that the company’s stock is overvalued and estimate IHS Markit’s valuation to be around $75, which is roughly 5% below the current market price. Our price estimate takes into account the most recent earnings as well as the company’s guidance for the current fiscal year.

Below we provide a detailed explanation of the key factors that could impact the company’s valuation.

Fiscal Q4 2019 Earnings Recap, and FY 2020 Guidance

- IHS Markit delivered yet another strong performance for its fiscal fourth quarter (ending November 2019).

- The company’s total revenue increased by 5% year-over-year, driven by a 5% increase in the Financial Services segment and a 9% growth in the Transportation division, partially offset by an 8% decline in the CMS business.

- Moreover, adjusted earnings per share increased by 14% to $0.65 per share, compared to $0.57 reported in the year-ago quarter.

- IHS Markit also provided an upbeat outlook for full-year 2020.

- The company expects organic revenue to increase in the range of 5-6%, with total revenue falling in the range of $4.52 billion to $4.59 billion.

- Additionally, the company expects adjusted EBITDA to be in the range of $1.86 billion to $1.89 billion.

Read Also: How To Run A Startup Part-Time Without Working Over Time

#1 Financial Services is IHS Markit’s Most Valuable Business

- Financial Services segment has achieved robust growth in the last few years, with revenues increasing from around $450 million in 2016 to more than $1.7 billion in FY 2019 (ending November) at an average annual rate of 56%.

- This growth was primarily driven by the merger of IHS with Markit in 2016. Since then, organic growth has been complemented by the acquisition of Ipreo. Moreover, during the year, the company expanded its pricing and reference data and valuations offerings, successfully launched new regulatory solutions, and launched several new indices – further aiding the segment’s growth in 2019.

- We expect this segment to sustain its growth, with revenues increasing at a rate of 4% to more than $1.75 billion in FY 2020 likely to be driven by the index business, Ipreo, and growing compliance requirements in the financial services industry.

- Notably, the division has continued to witness strong organic growth, with the division recording an organic growth of 6% over 2018-2019.

- As a result of the strong organic and acquisitive growth, the division’s contribution to total revenues has more than doubled from 16% in 2016 to 39% in 2019.

#2 Transportation Division Holds Strong Growth Potential

- Transportation segment is one of the fastest-growing segments, adding well over $350 million to total revenue since 2016 at an average annual rate of 11.8%.

- This segment grew by 7.4% y-o-y in 2019, adding $86 million to total incremental revenues led by the successful launch of its new product, CARFAX, which helps dealers better target their service line marketing.

- In 2020, the transportation division’s organic growth is expected to be in the single-digits, driven by strong recurring revenue performance. Additionally, the company’s used car business will also continue to see strong results from used car listings, its banking and insurance products, and the company’s new CARFAX for Life product.

#3 Performance of Consolidated Markets & Solutions Segment Is A Cause For Concern

- CMS segment has failed to achieve any growth over 2016-19, with the company’s revenues remaining stagnant at $532 million over the period.

- This segment weighed on the company’s performance in 2019, with the division losing over $20 million in revenues mainly due to the divestiture of the company’s market research business within the Media & Telecom business.

- Moreover, this is the company’s least profitable segment with an adjusted EBITDA margin of 22.1% as compared to the company’s overall margin of 40.3%.

- For FY 2020, IHS expects the division’s performance to improve and achieve low- to mid-single-digit organic growth.

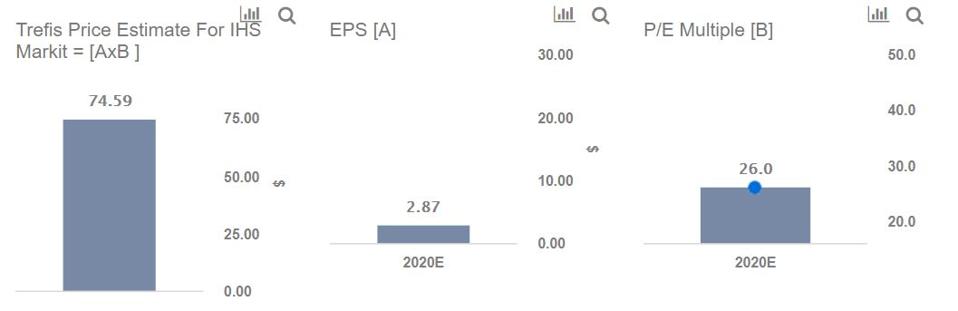

Per Trefis estimates, IHS Markit’s adjusted EPS for 2020 is likely to be $2.87. Taken together with a P/E multiple of 26x, this works to a fair value of $75 for IHS Markit’s stock, which is roughly 5% behind the current market price.

We highlight how IHS Markit’s P/E multiple has trended over the years, and compare this key metric with that for its peers Intercontinental Exchange, CME Group, and Nasdaq in our interactive dashboard.

FORBES