Intel Corporation is rising again on Wall Street, but it’s still trying to catch up with its main chip rival Advanced Micro Devices.

Intel’s shares are up 46.39% over the past twelve months compared to 154.29% of AMD.

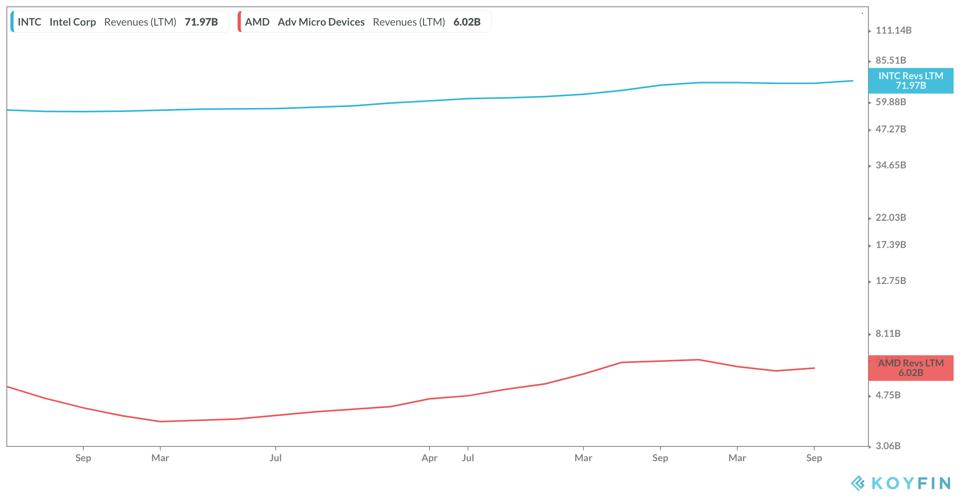

Intel is the largest U.S. chipmaker, about ten times the size of Intel in terms of revenue.

koyfin_20200125_075554728

KOYFIN

koyfin_20200125_081840083

KOYFIN

Last week, the chipmaker reported adjusted EPS of $1.52 for the fourth quarter, up from $1.28 a year earlier. Sales gained 8% to $20.21 billion.

Sales gains extended across almost every product line, including the company’s traditional market segment, which makes chips that power personal computers, confirming a recovery in the chip industry.

“Intel’s 4Q earnings report addresses the market’s concerns that the recovery in chip demand had been faltering,” says Haris Anwar, an analyst at financial markets platform Investing.com. “The largest chip producer in the U.S., not only beat expectations for the last quarter but also produced firm guidance for this coming year.”

Intel’s strong report further confirms that the company’s restructuring plan that began a few years ago is working. That’s especially the case for its cloud-computing industry, which has been experienced substantial growth in recent years.

“The report also shows its products which cloud-computing vendors use to build up big data centers, are in great demand and contributing strongly to the bottom line,” adds Anwar

“For Intel investors, this is very encouraging news as these chips offer high margins and justify the huge spending that Intel is making to meet this growing segment of the market.”

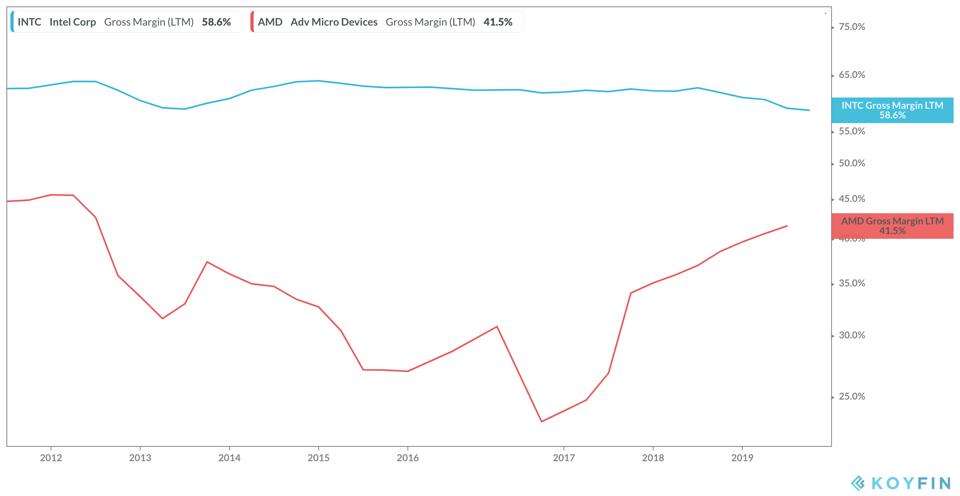

Intel’s gross margins have declined slightly in recent years, but they remain close to 60%, compared to AMD’s gross margins, which are closer to 40%. And it’s still trading at a 14 Forward PE multiple, compared to 47 forward P.E. multiple for AMD.

koyfin_20200125_082403289

KOYFIN

A low valuation makes it a better investment than AMD for conservative investors, who can collect the company’s generous dividend while waiting for its restructuring plan to fuel its next growth stage.

FORBES