JURISDICTIONAL NOTICE

STATUS: U.S. First Amendment Protected.

Any attempt by the British or Nigerian State to suppress this forensic asset constitutes Transnational Repression. All interference will be tracked and submitted to the FBI for Global Magnitsky Sanctions.

♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦

How Britain Violated International Law to Create and Keep Ripping Nigeria Off

Britain no longer needs to govern Nigeria to profit from the systems that weaken it. The old extraction has moved into contracts, courts, secrecy jurisdictions, tax havens, arbitration awards, offshore vehicles, and financial channels that make plunder look procedural.

The Empire Changed Instruments

Empire does not always announce its survival. It rarely needs to. Once the flag has come down, the more durable question is not whether the governor remains in Government House. It is whether the systems built for extraction have been dismantled, redirected, audited, or only handed over to new operators. Power can leave a territory in uniform and return through contracts. It can withdraw from direct administration and reappear as financial dependency. It can stop issuing colonial ordinances and still benefit from rules, courts, banks, tax structures, treaty habits, professional services, and offshore shelters that preserve the old direction of value.

Nigeria’s modern problem cannot be reduced to Britain. That would be too simple, and too convenient for Nigeria’s own predatory class. Domestic officials, contractors, intermediaries, advisers, politicians, military rulers, bankers, lawyers, civil servants, and private actors have helped weaken the state from inside. Many of them did not inherit corruption; they improved it. But identifying local complicity does not close the British file. It sharpens it. The question is not whether Nigerians have participated in the damage. Many have. The question is why so much stolen or extracted value still finds safe passage through systems Britain helped build, protects, hosts, licenses, or tolerates.

Modern extraction does not need a colonial office. It needs enforceable paperwork. It needs an offshore company. It needs a contract drafted with asymmetry buried in the clauses. It needs legal venue, arbitration language, beneficial ownership opacity, tax sheltering, professional respectability, bank accounts, advisers, nominees, and courts capable of transforming private claims into pressure against a sovereign treasury.

The visible event is usually narrow: a contract dispute, a tax arrangement, an asset recovery case, a shell company, a suspicious property purchase, a consultancy invoice, a judgment debt, a procurement scandal, a deferred investigation. The hidden structure is wider. Money leaves weak institutions and enters stronger legal systems. Once inside those systems, the money acquires documents, lawyers, confidentiality, jurisdiction, investment language, and distance from the public that lost it. This is the point at which theft stops looking like theft and begins to look like a file.

Britain’s relevance lies here. It sits at the center of a legal-financial world that has learned how to receive value without asking enough questions about the conditions that produced it. The City of London, British-linked offshore jurisdictions, professional services, commercial courts, arbitration culture, property markets, and secrecy networks form a continuing field of advantage. Not every transaction inside that field is illicit. That is not the claim. The claim is more precise: systems that make opacity profitable and enforcement sophisticated are especially dangerous to states already weakened by colonial inheritance, elite capture, and institutional underdevelopment.

Read also: Britain’s Imperial Fraud: Part 6

The Spider’s Web Is Not a Metaphor

The Tax Justice Network describes the United Kingdom, together with its Overseas Territories and Crown Dependencies, as the “UK spider’s web,” a network in which satellite jurisdictions facilitate profit shifting and illicit financial flows, with the City of London sitting at the center of global money movement. That description matters because it identifies a system, not an accident. The old empire did not simply lose its territories; parts of its post-imperial network became useful to global capital. The same political tradition that once moved goods through imperial ports now helps move value through legal and financial channels that are difficult to see and harder to tax.

A state like Nigeria does not need to be colonized again to be drained. It only needs weak public institutions at one end and sophisticated financial absorption at the other. The money may travel through companies, trusts, nominees, real estate, consultancy payments, capital flight, transfer pricing, under-invoicing, over-invoicing, politically exposed accounts, or legal settlements. By the time it reaches a respectable jurisdiction, the language changes. Loot becomes investment. Extraction becomes tax planning. Concealment becomes privacy. Intermediation becomes service.

That change of language is not cosmetic. It is operational. Systems survive by naming themselves carefully. A tax haven rarely introduces itself as a tax haven. It calls itself a financial center. A secrecy structure calls itself asset protection. A shell company calls itself a vehicle. A predatory clause calls itself contractual certainty. A judgment debt calls itself enforcement. The violence is not removed; it is translated.

Tax Abuse as Sovereignty Loss

Tax is not a technical inconvenience. It is the state’s ability to convert private economic activity into public capacity. When taxes are stripped, shifted, hidden, deferred, or routed through havens, a country does not merely lose revenue. It loses hospitals, roads, courts, schools, salaries, water systems, investigative capacity, regulatory enforcement, and bargaining power. The damage is not theoretical. It lands as underfunded institutions and then reappears as proof that the country is incompetent.

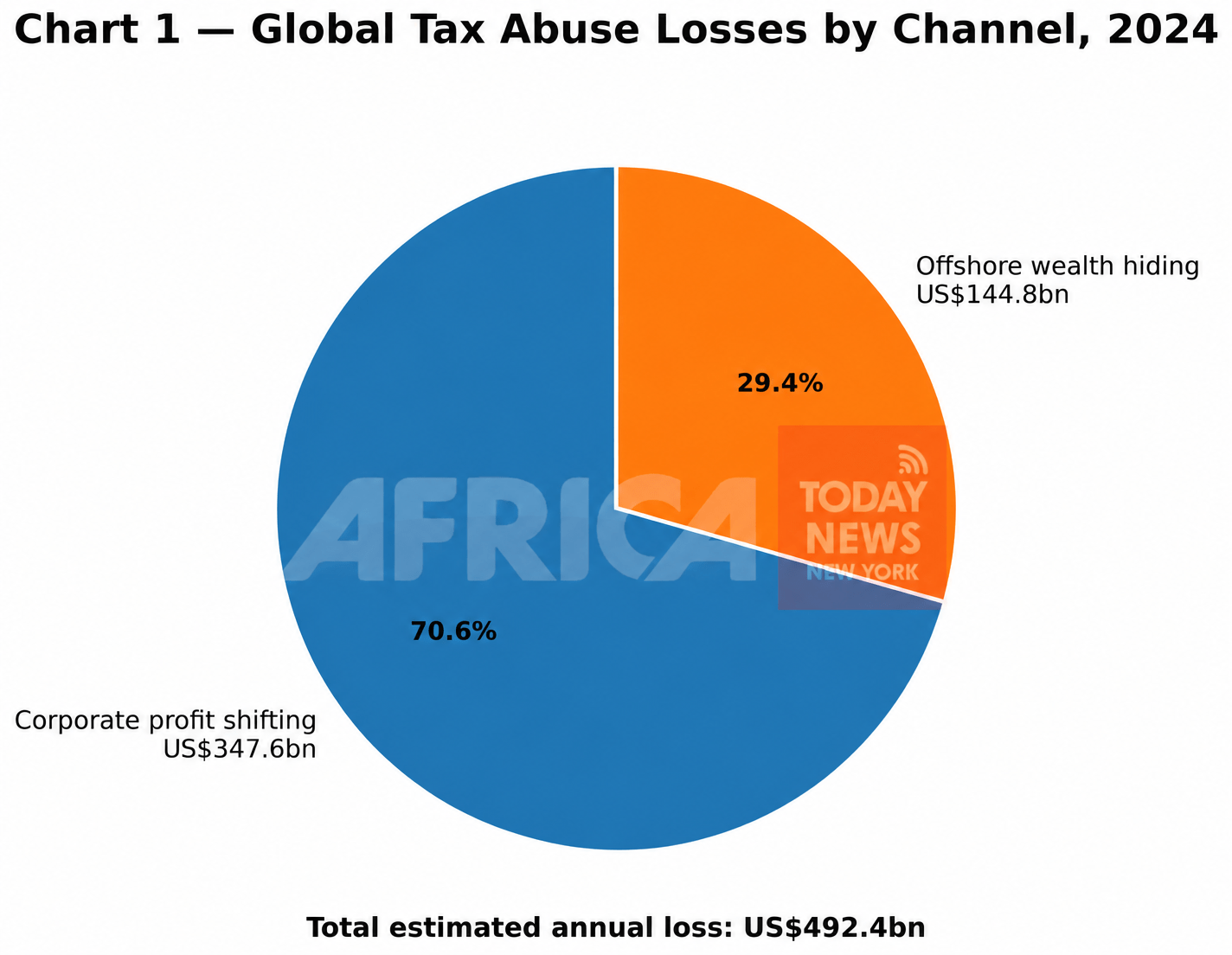

The Tax Justice Network’s State of Tax Justice 2024 estimated that countries lose US$492 billion a year to global tax abuse, with US$347.6 billion lost to multinational corporations shifting profit offshore and US$144.8 billion lost to wealthy individuals hiding wealth offshore. The same report identified the United Kingdom among eight countries opposed to a UN tax convention and stated that nearly half of global losses were enabled by those countries.

Chart 1 Explanation

This pie chart breaks down the estimated US$492.4 billion in annual global tax losses into two channels: corporate profit shifting and offshore wealth hiding. The dominant share is corporate profit shifting, at US$347.6 billion, or about 70.6% of the total. Offshore wealth hiding accounts for US$144.8 billion, about 29.4%.

The value of this chart is that it makes the structure of the drain visible. Global tax abuse is often discussed as if it were a vague technical problem, but the chart shows that the largest loss comes from corporations shifting profits away from the places where real economic activity occurs. That means factories, consumers, labor, natural resources, and markets may sit in one country while taxable profit is booked somewhere else. The injury is not abstract. It reduces the revenue available for hospitals, schools, infrastructure, courts, security, salaries, and public administration.

Tax Abuse as Sovereignty Loss — Continued

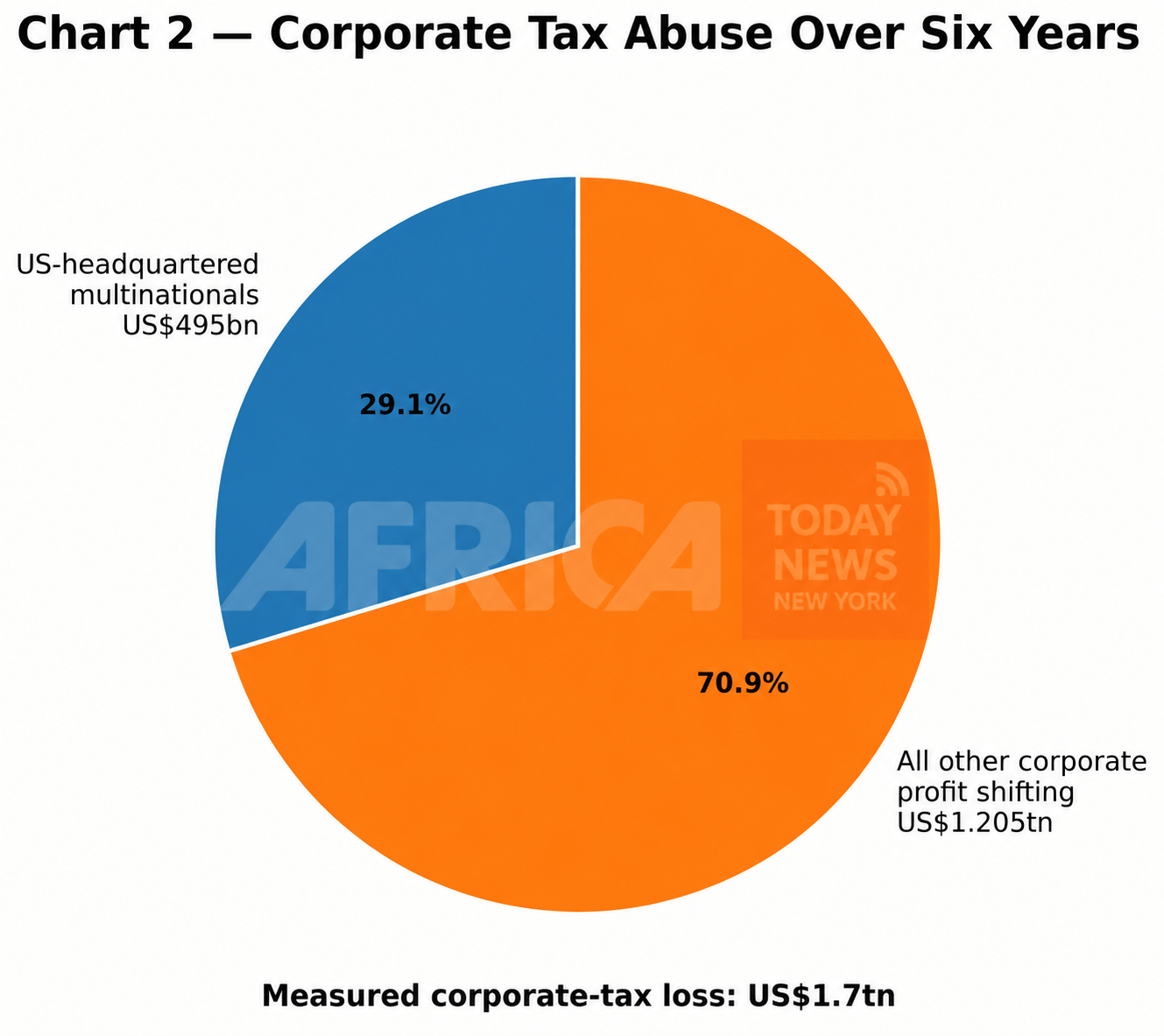

The 2025 report sharpened the picture through corporate tax abuse data. Over the six-year period for which data were available, US-headquartered multinationals alone were responsible for about US$495 billion in corporate tax losses worldwide, roughly 29 percent of the global corporate-tax abuse total of US$1.7 trillion. That figure is not about Nigeria alone, and it should not be misused as though it were. Its importance is structural. It shows the size of the global system in which developing states attempt to finance public life while mobile capital uses secrecy, mismatched reporting, treaty gaps, and profit shifting to reduce its obligations.

Chart 2 Explanation

This chart isolates corporate tax abuse over a measured six-year period. It shows that US-headquartered multinationals account for about US$495 billion, or 29.1%, of the estimated US$1.7 trillion in corporate tax losses. The remaining US$1.205 trillion, or 70.9%, is attributed to all other corporate profit shifting.

The chart should not be read as a Nigeria-only figure. Its importance is structural. It shows the scale of the global system in which developing countries are forced to operate. When multinational profit can be shifted across borders at this magnitude, weaker states lose revenue not because they have no economy, but because the rules allow profit to escape the places where value is created. That is the forensic point: the loss is produced through systems that appear lawful, technical, and routine.

Tax Abuse as Sovereignty Loss — Continued

Nigeria’s injury sits inside that system. A state built for extraction, then handed independence without full institutional reconstruction, now competes in a financial order where wealth can leave faster than public authority can trace it. The old colonial problem was that Britain controlled the port. The modern problem is that the exit point may be a spreadsheet, a transfer-pricing policy, a beneficial ownership structure, a London property transaction, a British Virgin Islands company, a Cayman vehicle, a Jersey trust, a professional opinion, or an arbitral award.

The UN Tax Fight Reveals the Fault Line

The struggle over the United Nations Framework Convention on International Tax Cooperation is not a technical disagreement between tax specialists. It is a contest over who gets to write the rules of extraction and public finance. The UN process aims to build a more inclusive global tax system through a framework convention and early protocols, including work on cross-border services income and tax dispute prevention and resolution. The fourth session of the Intergovernmental Negotiating Committee met in New York from 2 to 13 February 2026, with final texts expected to move toward the General Assembly process by 2027.

That timetable matters because it shows the battlefield shifting. For decades, global tax rulemaking has been dominated by wealthy states and forums where developing countries entered late, weak, or as recipients of rules largely shaped elsewhere. The UN process challenges that arrangement by placing all member states at the table. Whether it succeeds is uncertain. The resistance is predictable. Countries that benefit from the existing order rarely describe their position as defense of advantage. They describe it as legal certainty, investment stability, technical coherence, avoidance of double taxation, or protection of existing treaty networks.

Those phrases should be read carefully. Legal certainty for whom? Stability for whose capital? Coherence in whose favor? A system can be legally certain and still unjust. It can be stable because the losses are exported to weaker states. It can be coherent because the rules have been written to make certain forms of extraction difficult to challenge. The question is not whether tax rules should be orderly. They should. The question is whether order is being used to protect public revenue or to preserve private escape.

P&ID: The Paper Raid

If the tax system shows the slow drain, P&ID shows the attempted strike. The case is not useful because it proves every foreign investor is predatory. It does not. It is useful because it shows how a sovereign state can be placed under enormous pressure through paper, venue, arbitration, interest, procedure, and professional machinery.

In 2010, Nigeria entered into a gas supply and processing agreement with Process & Industrial Developments Ltd. The project did not proceed. Arbitration followed. P&ID obtained awards that rose to approximately US$6.6 billion plus interest, and by the time the dispute reached its most dangerous point the amount was widely reported at about US$11 billion. In 2023, the English High Court set aside the awards, finding that they had been obtained by fraud and procured contrary to public policy. Reporting and legal summaries noted false evidence, bribery of a Nigerian official, and improper retention of Nigeria’s privileged legal documents.

The facts should be read without melodrama. A contract was signed. The project failed. Arbitration was used. A huge award emerged. The award grew with interest. Enforcement threatened a state. A court later found fraud. That sequence is enough. The danger lies in the distance between the apparent form and the hidden contamination. On the surface, P&ID looked like a commercial dispute. Beneath the surface, the English court found misconduct serious enough to destroy the award. The paper was not neutral. It carried a trap.

P&ID was not colonialism in uniform. It was something more modern: a sovereign state almost bled by documents. No gunboat was required. No governor issued an order. The pressure came through contract, arbitration, jurisdiction, legal fees, enforcement threat, and accrued interest. That is why the case belongs in this series. It shows the updated method. Empire once required territory to extract. Modern systems can threaten extraction through enforceable claims against the treasury.

The Costs Dispute Shows the Afterlife of the Fight

Even after Nigeria defeated the award, the struggle did not end. In 2025, the UK Supreme Court addressed the currency of costs payable after Nigeria’s successful challenge. P&ID argued for costs in naira, which would have reduced the practical value of the award because of currency depreciation. The Supreme Court rejected that position and held that costs should normally be awarded in the currency in which the successful party incurred and paid them; Nigeria’s legal costs had been billed and paid in sterling, so sterling was the correct currency.

The point is not that the Supreme Court acted against Nigeria. It did not. On that issue, Nigeria prevailed. The point is the forensic pattern. After an award procured by fraud had collapsed, another dispute emerged over whether Nigeria’s currency weakness could reduce the monetary consequences for the party that had lost. The case shows how a sovereign injury can multiply inside legal process. First comes the contract. Then arbitration. Then enforcement. Then the challenge. Then costs. Then currency. Each stage has its own technical language. Each stage consumes time, public money, legal attention, and administrative capacity.

A rich state can absorb such litigation as part of doing business. A weaker state bleeds attention. That difference matters. Legal process can be legitimate and still become a site where unequal capacity is exposed. Nigeria won the P&ID battle, but the fact that the battle had to be fought at that scale is itself evidence of vulnerability.

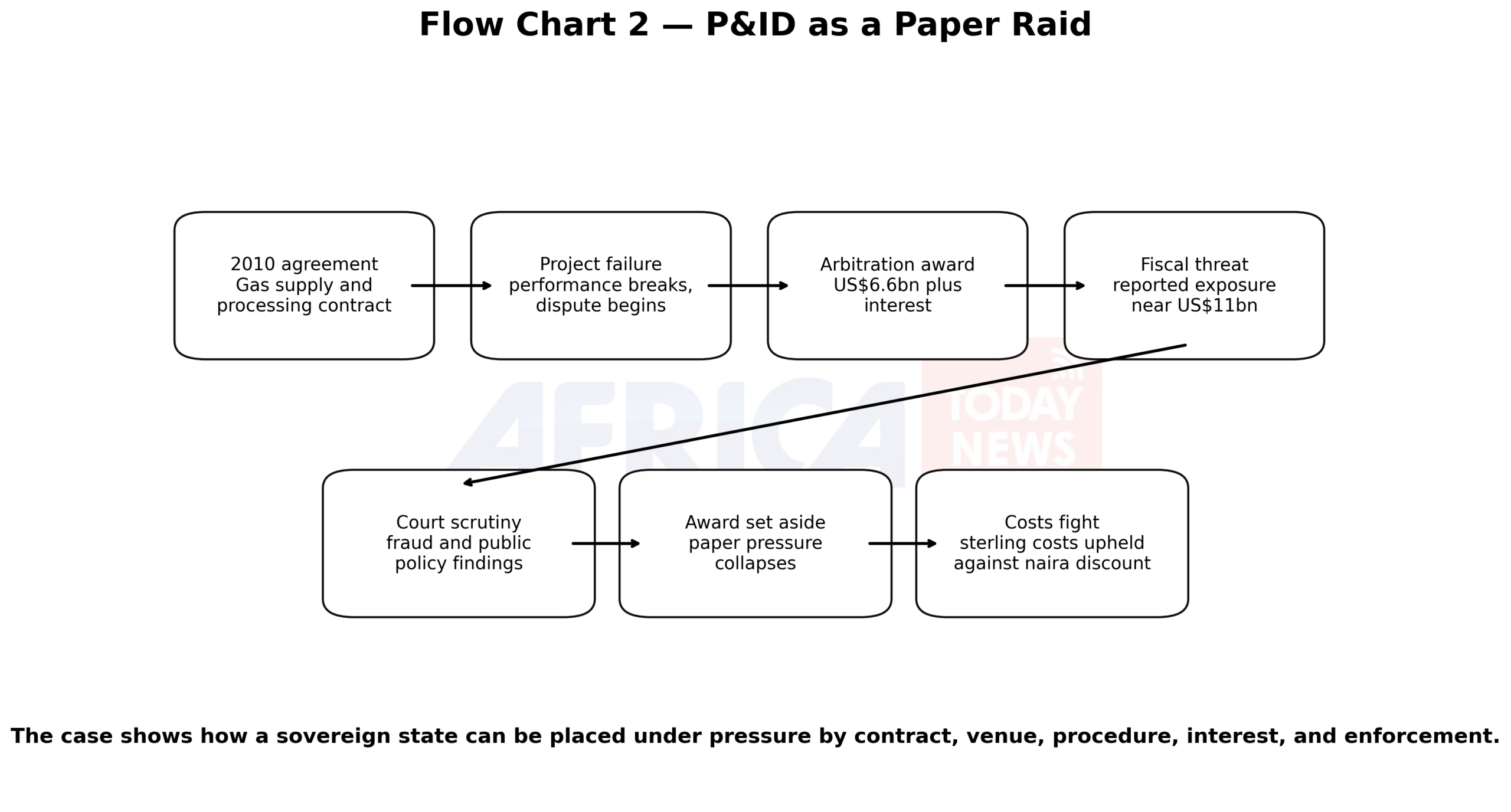

Flow Chart 2 Explanation

This flow chart reduces the P&ID case to its essential sequence. It begins with the 2010 gas supply and processing agreement, then moves to project failure, followed by an arbitration award of US$6.6 billion plus interest. That award created a reported fiscal threat near US$11 billion. The chain then moves into court scrutiny, where fraud and public-policy findings became central. The award was eventually set aside, but the process did not end there. A further costs dispute followed, including the question of whether costs should be paid in sterling rather than reduced through naira depreciation.

The chart matters because it shows how a sovereign state can be attacked through procedure. The P&ID case was not an invasion, a blockade, or a direct seizure of assets. It was pressure through contract, arbitration, interest, legal venue, enforcement risk, privileged documents, and litigation costs. That is why the article describes it as a paper raid. The weapon was not military power. The weapon was enforceable paperwork.

The Local Collaborator Is Not a Footnote

No external drain works efficiently without internal openings. P&ID was not possible because of foreign actors alone. The English court’s findings included bribery involving a Nigerian official. That fact must not be softened. Nigeria’s own public institutions were breached. Officials and insiders who assist predatory arrangements are not secondary characters. They are the bridge between external opportunity and national loss.

But collaboration does not absolve the external system that receives, enforces, structures, or dignifies the claim. Both sides must remain visible. The internal actor opens the gate. The external machinery gives the transaction reach. The local corrupt official may sign the paper; foreign professionals may draft, defend, finance, arbitrate, enforce, insure, or launder the benefit. A serious investigation does not choose one side of the chain. It follows the chain.

That is where many public debates fail. Some reduce everything to foreign exploitation. Others reduce everything to Nigerian corruption. Both readings protect someone. The first protects domestic predators. The second protects international systems of advantage. The evidence points to a more uncomfortable conclusion: Nigeria is damaged by the meeting point between local betrayal and global machinery.

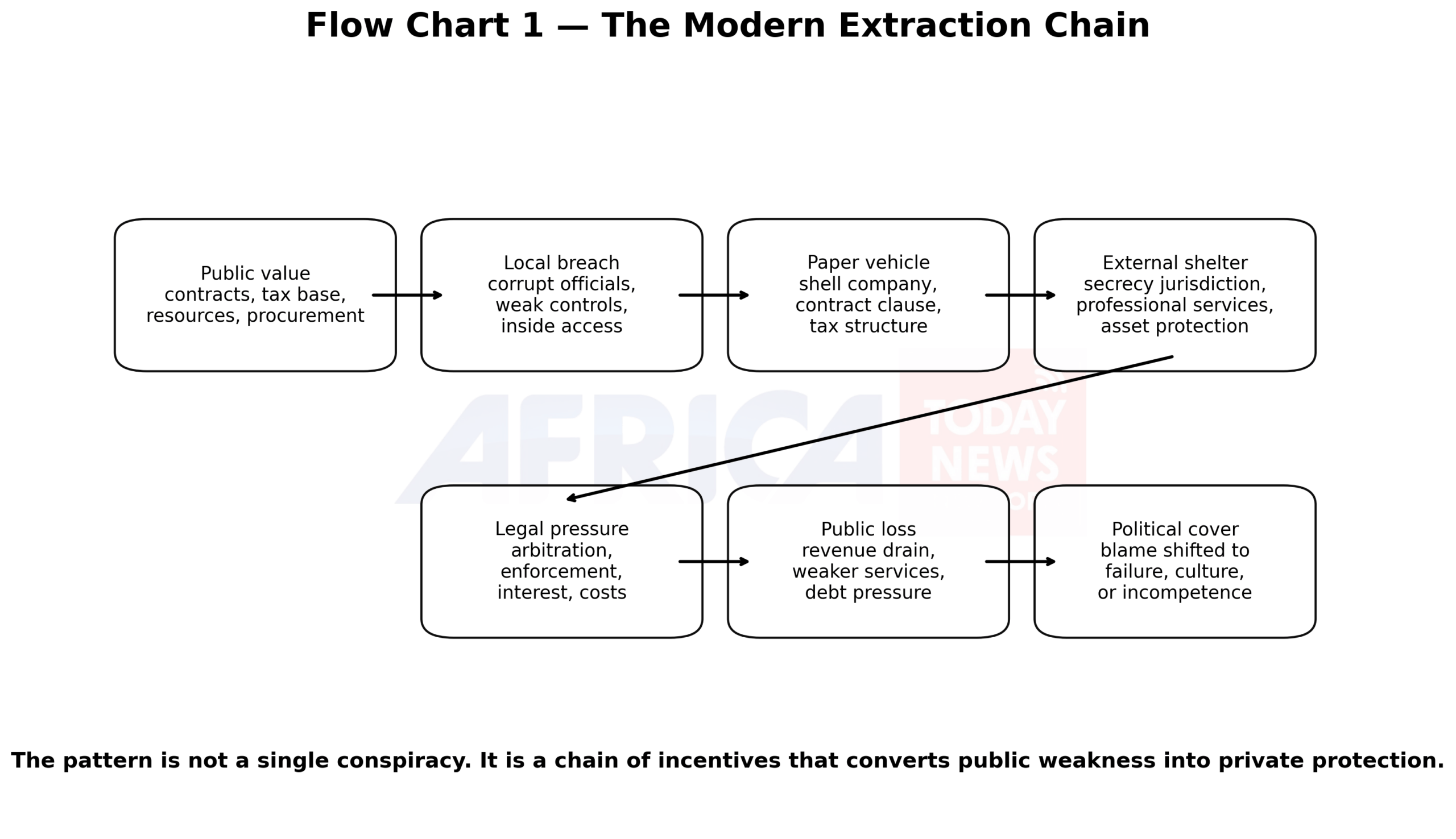

Flow Chart 1 Explanation

This flow chart explains the operating sequence of modern extraction. It begins with public value: contracts, tax base, resources, procurement, or sovereign assets. That value becomes vulnerable through a local breach: corrupt officials, weak controls, inside access, compromised institutions, or negligent public administration. The breach is then converted into a paper vehicle through shell companies, contract clauses, tax structures, invoices, trusts, or special-purpose entities.

Once the paper vehicle exists, value can move into an external shelter: secrecy jurisdictions, professional services, asset-protection structures, banks, property markets, or arbitration-friendly venues. From there, pressure can return to the state through legal mechanisms such as arbitration, enforcement, interest, legal costs, or judgment debt. The final injury is public loss: revenue drain, weaker services, debt pressure, institutional distraction, and reduced public capacity. The political ending is familiar: blame is shifted to failure, culture, incompetence, or corruption alone, while the external machinery fades from public view.

This chart is important because it avoids a simplistic argument. It does not say extraction is caused only by Britain or only by Nigerian corruption. It shows the chain between internal breach and external machinery. That is the strongest forensic position: local betrayal opens the gate; global systems give the transaction protection, distance, and enforceability.

Secrecy Is the Operating Condition

The modern fleece depends on opacity. Without opacity, extraction becomes harder to disguise. Beneficial ownership secrecy hides who controls companies. Tax secrecy hides where profit is booked. Arbitration confidentiality can hide public-interest disputes from scrutiny. Legal privilege can be abused if documents are improperly obtained or retained. Property ownership layers can hide politically exposed money. Professional gatekeeping can turn suspicion into billable work.

The Financial Secrecy Index is useful because it measures how jurisdictions enable concealment of ownership and financial information and how much cross-border financial activity they provide. In its 2025 ranking, the United Kingdom appeared among the top financial secrecy jurisdictions, while the Cayman Islands also ranked highly. That matters not because every transaction through those jurisdictions is corrupt, but because secrecy environments expand the surface area for abuse.

Nigeria’s public money does not disappear into the air. It travels through mechanisms. Some are domestic. Some are global. Some are legal. Some are illegal. Some are legal because the law has been written to tolerate what justice should not. The task of forensic inquiry is not to shout “theft” at every complexity. It is to identify where complexity repeatedly serves the same outcome: public loss, private insulation, and institutional helplessness.

Why Britain Remains in the Dock

Britain’s defenders will say the empire ended. That is formally true. They will say Nigeria is sovereign. That is legally true. They will say Nigerian leaders have looted Nigeria. That is undeniably true. None of those truths resolves the question. Formal sovereignty does not erase financial dependency. Legal independence does not dismantle offshore secrecy. Domestic corruption does not absolve foreign reception systems. The end of colonial rule does not end responsibility for networks that continue to profit from the vulnerabilities empire helped create.

A serious indictment does not require claiming that Britain controls everything. It requires showing that British-linked systems remain central to many of the pathways through which value can leave countries like Nigeria and acquire protection elsewhere. The UK spider’s web, the role of the City of London, the standing of English law, the attraction of English courts, the use of British-linked offshore territories, and the global prestige of British professional services are not marginal facts. They are part of the terrain on which modern extraction operates.

The question is not whether Britain signs every transaction. The question is whether Britain continues to benefit from systems that make extraction easier and accountability harder. That is a different charge, and a harder one to escape.

The Pattern Beneath the Cases

When the evidence is placed in sequence, the modern fleece becomes easier to see. Tax abuse reduces sovereign capacity. Offshore secrecy hides ownership and movement. Arbitration can convert private claims into public fiscal threat. English legal systems can become central venues for enforcing or dismantling those claims. Professional services can give dubious transactions polish. Domestic elites provide entry points. Public institutions carry the cost. Citizens experience the loss as poor hospitals, weak schools, collapsing roads, unpaid workers, fragile courts, insecure communities, and debt.

The pattern is not a single conspiracy. It is more durable than conspiracy. It is a system of incentives. Lawyers are paid to argue. Banks are paid to move money. Company agents are paid to incorporate. Tax advisers are paid to minimise liabilities. Arbitrators are paid to decide disputes. Property markets welcome capital. Politicians enjoy donations, influence, or silence. Weak states lack the resources to investigate fast enough. Strong jurisdictions insist on procedure. The result is not always illegal, but the direction is consistent: value moves away from public need and toward private protection.

That is why the language of “development failure” is inadequate. Nigeria is not only failing to build. It is being drained while trying to build. It is not only misgoverned from within. It is exposed to systems from without. Its public institutions are asked to perform under conditions in which resources, talent, evidence, and bargaining power can be extracted, hidden, or litigated away.

The Modern Fleece

The modern fleece does not look like the colonial fleece because it has learned to survive scrutiny. It does not usually arrive with a flag. It arrives with clauses. It arrives through debt, arbitration, secrecy, tax planning, transfer pricing, shell companies, investment treaties, legal opinions, consultancy contracts, and enforcement proceedings. It is cleaner on paper because the paper has become the weapon.

Britain’s imperial fraud therefore did not end at independence. It adapted. The old drain through the port became a drain through the financial system. The old company charter became the offshore vehicle. The old imperial court became the commercial venue. The old customs gate became the tax treaty. The old colonial intermediary became the politically exposed facilitator. The old extraction report became the professional opinion.

No serious country can repair itself while refusing to examine those channels. Nigeria must confront its local predators. It must prosecute corruption, strengthen procurement, reform public contracting, protect legal documents, improve tax administration, publish beneficial ownership data, audit arbitration exposure, professionalise state litigation, and make secrecy more expensive than disclosure. But Britain and its network must also be named where they remain useful to the movement, concealment, defence, or enforcement of extracted wealth.

The Drain Stayed Open

Britain no longer needs to sit in Lagos to profit from Nigeria’s weakness. That is the point. Direct rule would be crude, expensive, and politically impossible. Modern advantage works better when it can deny intention. The money moves. The lawyers appear. The contract speaks. The company structure hides. The court enforces or corrects. The tax gap widens. The public treasury absorbs the loss. The citizens are told to blame corruption, incompetence, population, culture, or fate.

Some of those explanations contain truth. None is complete.

The deeper truth is harder. Nigeria was built for extraction, handed independence without full reconstruction, and then inserted into a global order where extraction no longer needs colonial administration to succeed. Britain’s role has changed from ruler to host, beneficiary, venue, adviser, shelter, and historical architect of a system whose tools still work. That is not an accusation built on emotion. It is what the pattern shows when the paperwork is read against the money.

The old flag came down. The drain stayed open. The injury now travels through documents, jurisdictions, markets, secrecy, and law. That is the modern fleece: empire after the flag, extraction after independence, and a country still paying for the machinery Britain left behind while British-linked systems remain available to those who know how to use them.

Selected Verified References — APA 7th Edition

Federal Republic of Nigeria v Process & Industrial Developments Ltd, [2023] EWHC 2638 (Comm).

Process & Industrial Developments Limited v The Federal Republic of Nigeria, [2025] UKSC 36.

Tax Justice Network. (2024). The state of tax justice 2024. Tax Justice Network.

Tax Justice Network. (2025). The state of tax justice 2025. Tax Justice Network.

Tax Justice Network. (2025). Financial Secrecy Index 2025. Tax Justice Network.

Tax Justice Network. (n.d.). The UK spider’s web. Tax Justice Network.

United Nations. (2026). UN negotiations enter key phase for fairer global tax system. United Nations.

United Nations Financing for Sustainable Development Office. (2026). Intergovernmental negotiations for UN Framework Convention on International Tax Cooperation. United Nations Department of Economic and Social Affairs.